By Dennis Bidwell

February 2017

As development offices in non-profits of all sizes and shapes turn greater attention to attracting, closing and selling real estate gifts, I’m finding more and more charities are particular interested in exploring retained life estate possibilities with their donors.

The basics:

- The owner(s) of a personal residence or agricultural property can donate that property to charity, retaining the right to use the property for the rest of their lives (or for a fixed period of time.) This is known variably as a retained life estate, a reserved life estate, donating the remainder interest in the property, or retaining a life tenancy in the property.

- Though title in the property changes hands, the “life tenants” retain full use and control of the property, with full responsibility for taxes, utilities, maintenance, etc.

- A clear and detailed written agreement is essential to spell out all the responsibilities and rights in such situations, including dealing with incapacity, vacating the property, etc.

- Despite continuing to live in or use the property, the donor is entitled to a charitable tax deduction in the year of the gift that is based on the appraised value of the property (adjusted for their life expectancy), the applicable IRS discount rate, and other factors.

Charitable deduction potential

As an indication of the extent of the possible deduction for making a property gift subject to a retained life estate, the following table shows approximate deduction percentages as a function of age (and assuming a discount rate of 1.8%). For example, a 76 year-old donating a $1,000,000 property, subject to a retained life estate, could anticipate a possible charitable tax deduction of approximately $740,000. (As in the case of other property gifts held for more than one year, the maximum charitable deduction in any given year is 30% of adjusted gross income, but with the ability to carry forward any unused deduction for up to five additional years.)

Single Life % Joint Lives %

56 49% 56, 54 38%

66 62% 66, 64 51%

76 74% 76, 74 65%

86 85% 86, 84 78%

96 92% 96, 94 88%

[Note: As interest rates rise, the deductions available for retained life estate gifts decline.]

Comparison with a bequest of the property

Whenever a client tells me of a donor whose bequest intention suggests that a residential or farm property will be coming to the non-profit through the estate, my advice is that they should schedule a visit soon to that donor in order to review the benefits of donating the property in question now, and retaining a life estate. Chances are that the property owner is not aware that they could accomplish their aim – having the property pass to the charity for sale after their death – through a retained life estate gift, rather than by bequest. They’re probably also not aware of the several major advantages to making the gift during one’s lifetime, principal among them being the tax deduction available when making the gift now, rather than at death. And there’s also the benefit (for some) of being recognized now for one’s generous gift, as opposed to recognition after death.

Those of us in the gift planning business cannot assume that a donor in such a situation will be aware of the retained life estate alternative through their attorney or accountant of financial planner. It rarely works that way. Rather, it generally falls to us, as gift planners representing non-profit organizations, to explain the whole menu of options for disposing of real estate, including the retained life estate.

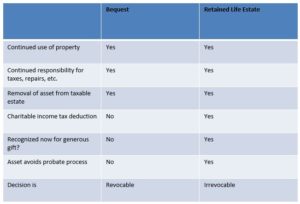

Here’s a comparison of leaving a property by bequest vs. leaving it now and retaining a life estate:

It’s not for every situation

A critical difference between donating the property now while retaining a life estate, as opposed to leaving the property through one’s will, is that the retained life estate arrangement is irrevocable (thus making available a charitable tax deduction.) One can always change one’s will. Not so with a retained life estate. Which means that anyone considering such a gift arrangement should think very carefully about it and seek expert professional advice. It also means that those of us who are gift planners should be aware that this is a gift arrangement only suitable for donors with sufficient financial resources to get through their retirement years without needing the real estate in question.